Learn more about our unique process with whole life insurance and how you can utilize it as a powerful asset! – …

Overfunding a whole life insurance policy is a strategic financial move that can provide numerous benefits for policyholders. By contributing more money than the required premium payments, policyholders can build cash value at an accelerated rate and potentially achieve more attractive returns on their investment.

What is overfunding a whole life insurance policy?

Whole life insurance is a type of permanent life insurance that offers both a death benefit and a savings component known as cash value. When policyholders pay their premiums, a portion of the money goes towards the death benefit, while the rest is allocated towards building cash value.

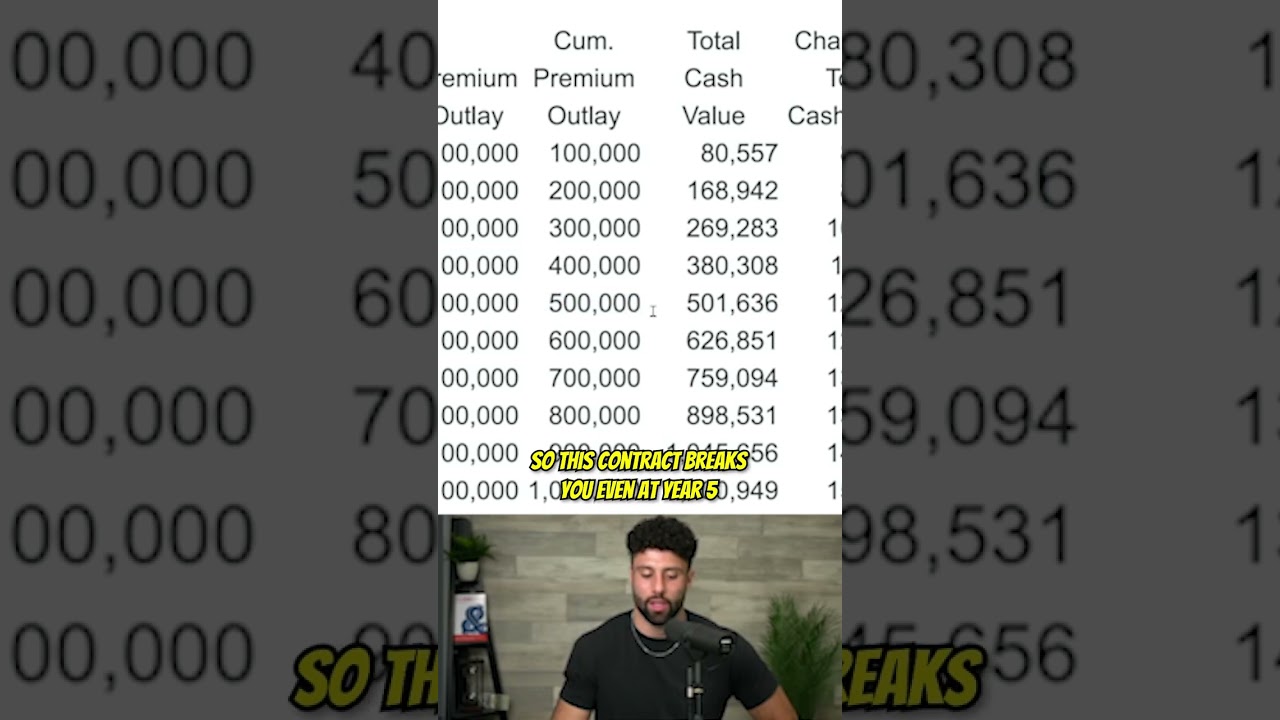

Overfunding a whole life insurance policy involves contributing more money than the required premium payments. This additional funding is deposited directly into the cash value portion of the policy, allowing it to grow at a faster rate than if only the minimum premium payments were made.

What are the benefits of overfunding a whole life insurance policy?

1. Accelerated cash value growth: By overfunding their policy, policyholders can build cash value more quickly. This can provide them with a valuable source of liquidity that can be accessed through loans or withdrawals for various financial needs, such as funding a child’s education, starting a business, or supplementing retirement income.

2. Enhanced death benefit: The cash value of a whole life insurance policy can be used to purchase paid-up additional insurance coverage, which increases the death benefit of the policy. By overfunding their policy, policyholders can maximize the death benefit, providing greater financial protection for their loved ones.

3. Tax advantages: The cash value growth in a whole life insurance policy is tax-deferred, meaning that policyholders do not have to pay taxes on the earnings until they are withdrawn. By overfunding their policy, policyholders can take advantage of this tax-deferred growth and potentially reduce their tax liability in the long run.

4. Creditor protection: In many states, the cash value of a whole life insurance policy is protected from creditors in the event of bankruptcy or a lawsuit. By overfunding their policy, policyholders can shield more of their assets from potential creditors, providing an additional layer of financial security.

How to overfund a whole life insurance policy?

To overfund a whole life insurance policy, policyholders must first determine the maximum amount of additional funds they can contribute. This amount will depend on the policy’s guidelines and the individual’s financial situation. Once the amount is established, policyholders can make additional premium payments directly to the insurance company or set up automatic withdrawals from their bank account.

It is important for policyholders to regularly review their policy and cash value growth to ensure that they are on track to achieve their financial goals. Working with a financial advisor can also help policyholders optimize their contributions and make informed decisions about overfunding their whole life insurance policy.

In conclusion, overfunding a whole life insurance policy can be a smart financial strategy for building wealth, enhancing financial protection, and maximizing tax advantages. By contributing more money than the required premium payments, policyholders can accelerate the growth of their cash value and enjoy a range of benefits that can positively impact their financial future.

Frequently Asked Questions

How much does whole life insurance cost?

Whole life insurance typically costs $150-$300/month for $250,000 in coverage for a healthy 30-year-old. While more expensive than term life, it provides lifelong coverage and builds cash value that grows tax-deferred.

What is the cash value of whole life insurance?

Cash value is the savings component of a whole life policy that grows over time at a guaranteed rate. You can borrow against it, withdraw from it, or use it to pay future premiums. Cash value grows tax-deferred and typically becomes accessible after 3-5 years.

Can I borrow from my whole life policy?

Yes, you can borrow against your policy’s cash value at any time. Policy loans have low interest rates and don’t require credit checks. However, unpaid loans reduce your death benefit and may trigger tax consequences if the policy lapses.

Where can I compare whole life insurance quotes?

You can compare free whole life insurance quotes from 50+ providers right here on Life Quotes Web. Our comparison tool shows side-by-side rates in under 2 minutes — get your free quotes now.

Compare Free Whole Life Insurance Quotes Today

Get personalized rates from 50+ providers. No obligation, no medical exam required.

🛡️ Get Your Free Whole Life Insurance Quote →

🔒 256-bit SSL Encrypted | ⭐ 4.8/5 Rating | 🏆 50+ Providers